by: Dr. Ronnie H. Davis, Printing Industries of America

How will the economy and print markets perform in 2012 and 2013? Here’s our outlook:

The 2012-2013 Economy

At the current time, the economy is forecast to continue the slow recovery from the recession. While a return to recession is always possible, especially since the recovery has been slow, the most likely scenario is for economic growth of more than three percent over the next two years. The largest unknown, of course, is the outcome of the national elections of 2012 and its impact on federal tax and spending policies, both over the short and long term.

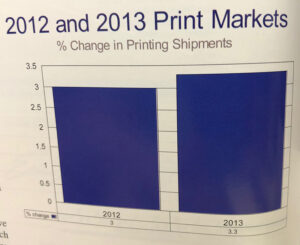

2012-2013 Print Markets

If the economy trends as projected, print markets should continue to grow. The 2012 national elections will provide an additional boost. All in all, our projection is for three percent growth in 2012 and 3.3 percent growth in 2013 on a nominal or non-inflation adjusted basis.

In terms of print function, the national elections should give a particular boost to marketing/promotional print, which means that this function would grow at above average rates. In contrast, print intended to inform/communicate will likely grow at a less than average pace. Print logistics will likely be in between these two.

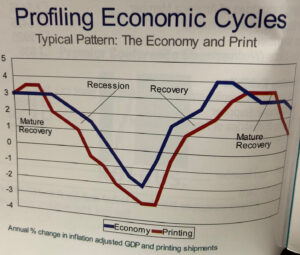

Strategy and Tactics for the Expected Economic Cycle

Strategy and Tactics for the Expected Economic Cycle

In designing strategies and tactics for the coming environment, keep in mind the key differences between print and the economy over a complete economic cycle:

- Although we project overall printing shipments adjusted for inflation to continue to grow, on average, for the next decade, they will likely grow less than the economy – perhaps around 1-1.5 percent less. For comparison purposes, we project the economy growing by around 2.5 percent and print by 1.5 percent for our composite cycle.

- Print generally leads recessions and lags recoveries, so that printing shipments turn down earlier as the recession begins and turn up slower once the economy recovers.

- Print does best when the economy reaches a mature recovery phase. In this sweet spot, print actually can outgrow the economy for a few quarters.

While printers and suppliers can’t do anything about the business cycle and these overall macroeconomic trends, they can help themselves by understanding this pattern as they manage:

- First, be aware of not only the current health of the economy and print markets, but also their respective positions in the cycle. Just as importantly, consider the emerging directions of both. Make sure that you take this into account before making any major business decisions, such as investment in new equipment or new business segment.

- Second, many operational decisions must be adjusted concurrent with the cycle. In particular, a focus on reducing fixed cost and making more costs variable with the business cycle is imperative. Don’t get caught with high fixed cost just as the cycle turns down.

- Third, print’s performance in bad economic times is in line with manufacturing as a whole and is actually not that bad compared to other manufacturing sectors. This does not make it any easier to cope, but at least there are plenty of industries and firms out there suffering as much or even more than print.

- Finally, remember to manage forward and not backward. While you have to be aware of past trends and manage for today, always remember that the cycle pattern will continue and the next up phase is coming.

Dr. Ronnie H. Davis is senior vice president and chief economist for Printing Industries of America. He can be reached via phone at 434.591.0527 or via email at rdavis@printing.org.