By Dr. Ronnie H. Davis, senior vice president and chief economist, PIA

With the New Year upon us, there is a dynamic mix of economic cross trends, politics, global trends and other issues. Presented below are the current views of Printing Industries of America (PIA) on print markets and the economy for the remainder of the year.

Mixed signals: Will the longest recovery keep going?

The $21 trillion US economy is a complex, dynamic amalgam of positive, stable and negative market forces. When upward forces dominate, we have growth. When downward forces dominate, we have recessions. Fortunately, over the past seven decades, upward forces have dominated more than 90% of the time, as they have over the last 126 months. Like the Energizer Bunny, the economy just keeps going and going and going, and it now stands as the longest continuous expansion in US history. Can it continue into 2020 and beyond?

The current economic expansion started all the way back in June 2009. This makes this expansion the longest in 164 years of record keeping by the National Bureau of Economic Research, the official scorer of the track of the economy.

US employment growth has averaged around 200,000 jobs per month – or about double the pace necessary to absorb growth in the working-age population. The labor force participation has risen almost steadily since the end of the recession, while the unemployment rate remains at a historic low. Wages are increasing at a modest pace, and there are more job openings than unemployed workers. The US manufacturing sector remains generally healthy, although it has experienced some weakness lately.

US employment growth has averaged around 200,000 jobs per month – or about double the pace necessary to absorb growth in the working-age population. The labor force participation has risen almost steadily since the end of the recession, while the unemployment rate remains at a historic low. Wages are increasing at a modest pace, and there are more job openings than unemployed workers. The US manufacturing sector remains generally healthy, although it has experienced some weakness lately.

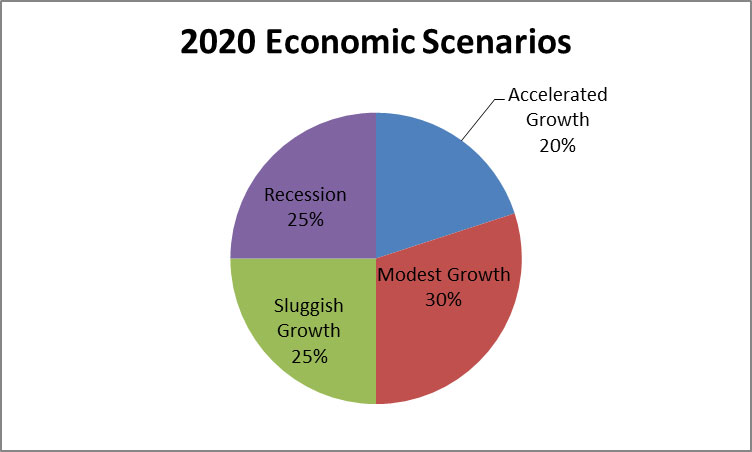

Looking into 2020, the economic outlook is even more cloudy than usual given the complex set of current circumstances discussed earlier. There are four distinct trajectories that the economy might take into 2020:

- Accelerated growth of 2.5% or more, with a slight uptick in growth over this year

- Modest growth with a return to the growth rates of 2017 (around 2%)

- Sluggish growth with a significant decline in growth, but no recession (around 1%)

- A 2020 recession beginning in the early part of the year and running through most of the year (a decline of around 1% to 1.5%)

Additional outcomes always are possible, but these four scenarios cover the logical options. Each of the four scenarios has a somewhat similar likelihood of happening, with modest growth slightly higher and accelerated growth slightly lower.

Outlook for print in 2020

Since the end of the Great Recession in June 2009, print markets have become increasingly strong. As we have previously pointed out, there are six key reasons why print and printers have largely been healthy since the end of the recession.

Since the end of the Great Recession in June 2009, print markets have become increasingly strong. As we have previously pointed out, there are six key reasons why print and printers have largely been healthy since the end of the recession.

On a nominal basis, print markets are growing around 1% to 2% at the present time. For 2018 (the most current data from the US Census), print’s economic footprint totaled $171.4 billion in annual shipments, around 42,000 establishments and more than 850,000 employees. Total print production increased by 3.6% last year.

Printers’ profits also are generally healthy, based on historical trends. PIA estimates that the average profit on sales for printers in 2018 was around 3%. Profit leading printers (those in the top quartile) earned around 9% on sales. Profit challengers (printers in the bottom three quartiles) earned only 1% on sales.

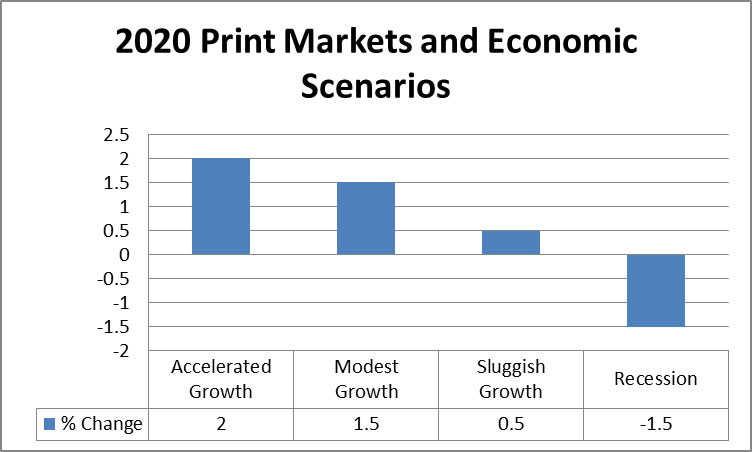

Print’s path over the next year depends primarily on the direction of the 2020 economy:

- Accelerated Growth. If the 2020 economy grows at an accelerated pace of 3% or more, printing shipments will increase by around 2% or more. This rate of growth will produce almost $3.5 billion in additional printing services in 2020.

- Modest Growth. If the 2020 economy grows at a modest pace of around 2%, print will grow by approximately 1.5%. This rate of growth will produce almost $1.7 to $2.6 billion in additional printing in 2020.

- Sluggish Growth. If the 2020 economy grows at a sluggish pace of only 1%, printing shipments will edge up only around 0.5%. This rate of growth will produce approximately almost $900 million in additional printing services in 2020.

- Recession. If the 2020 economy slides into recession, print will slide faster and further – likely falling by around 1.5% or more, depending on the exact timing of the recession. This will be a loss of close to $2.5 billion or more in printing shipments.

Not surprisingly, just as print sales track with GDP, printers’ profits track with print sales. Based on PIA Ratios data, printers’ profits are high when the growth rates of overall print sales are high. As the sales pace declines, profits fall and eventually move into negative territory as print sales growth approaches zero. If a recession takes place in the next year, print profits will fall substantially. Only profit leaders will end up in the black, with the typical printer breaking even and challengers in the red.