Submitted by the Paperboard Packaging Council

As the world began to move on from strict measures to control the spread of COVID-19, 2022 started to provide the first insights into what the ‘new normal’ would be. Stuck in quarantine and flush with stimulus cash, consumer spending on goods during the pandemic drove an unexpected surge in carton demand. Normalization trends have seen that spending shifting away from goods and back toward services. How will different end-use markets react to the shifting spending? What trends will drive carton shipments in the coming years?

The past year also has forced consumers to deal with levels of inflation unseen for decades. How will the market react to inflation many consumers have not seen in their lifetime? In this uncertain environment, understanding the underlying trends that drive the industry is more important than ever. This report provides a detailed examination of the US and Canadian carton markets, how they operate and the factors driving future trends. It also contains a deep dive into the 17 end-use markets that are the primary sources of demand for folding cartons, with an investigation into past and future trends for spending, trade, production and carton shipments to each end-use market. Additionally, the report includes key takeaways that summarize the study findings for the cartonboard market in the United States and Canada as well as for each of the end-use markets that drive carton demand.

Outlook summary

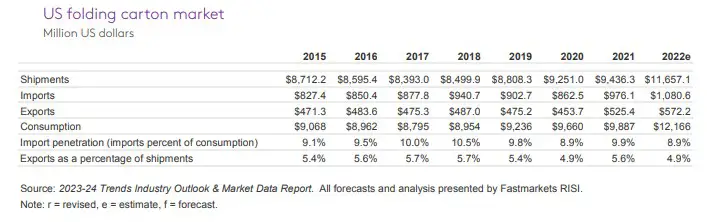

In 2022, as the world began to move past the COVID-19 pandemic, there were concerns about how markets would react as the economy moved toward a ‘new normal.’ Carton shipment growth had been in decline since the Great Recession. Prior to 2020, losses in shipments largely were the result of continued headwinds facing major processed food and consumer product companies. Processed food exports were challenged by the appreciation of the US dollar in 2015, which trickled down to recycled boxboard demand and folding carton shipments. Over the last decade (2010-19), folding carton shipments were under persistent downward pressure and declined at an average annual rate of 1.2%. Since the Great Recession, only four years have not experienced a decline in shipments: 2014, 2017, 2020 and 2021. When COVID-19 hit in 2020, industrial production dropped 7.2% and consumer spending fell 3%. Consumers, however, flush with stimulus money and stuck in lockdown, greatly increased their spending on goods, helping boost carton shipments to some of the strongest years in recent history. Carton shipments recorded extraordinary growth of 5.5% year on year in 2020. These gains were maintained in 2021 when shipments grew another 0.2%. With the remaining pandemic restrictions lifted in 2022, spending started to shift away from goods and back toward services, but strong inventory rebuilding throughout the supply chain helped push shipments up another 4.5%. While 2022 had the highest volume of carton shipments since 2010, it still was 8.7% below the pre-recession peak in 2007.

In 2022, as the world began to move past the COVID-19 pandemic, there were concerns about how markets would react as the economy moved toward a ‘new normal.’ Carton shipment growth had been in decline since the Great Recession. Prior to 2020, losses in shipments largely were the result of continued headwinds facing major processed food and consumer product companies. Processed food exports were challenged by the appreciation of the US dollar in 2015, which trickled down to recycled boxboard demand and folding carton shipments. Over the last decade (2010-19), folding carton shipments were under persistent downward pressure and declined at an average annual rate of 1.2%. Since the Great Recession, only four years have not experienced a decline in shipments: 2014, 2017, 2020 and 2021. When COVID-19 hit in 2020, industrial production dropped 7.2% and consumer spending fell 3%. Consumers, however, flush with stimulus money and stuck in lockdown, greatly increased their spending on goods, helping boost carton shipments to some of the strongest years in recent history. Carton shipments recorded extraordinary growth of 5.5% year on year in 2020. These gains were maintained in 2021 when shipments grew another 0.2%. With the remaining pandemic restrictions lifted in 2022, spending started to shift away from goods and back toward services, but strong inventory rebuilding throughout the supply chain helped push shipments up another 4.5%. While 2022 had the highest volume of carton shipments since 2010, it still was 8.7% below the pre-recession peak in 2007.

The COVID-19 pandemic and the associated recession saw spending shift from services to goods, which had a significant impact on folding carton shipments. While consumer spending in 2020 declined 3% and spending on services dropped 6.2%, nondurables spending increased 2.7%. In 2021, consumer spending rose 8.3%, with nondurables spending increasing 8.8%. Spending on services in 2021 saw a partial recovery, rising 6.3%. In 2022, spending grew 2.7% but began to shift toward services, which increased 4.5% for the year. While still elevated, non-durables good spending dipped 0.5% in 2022. Consumer spending on processed food witnessed strong growth of 5.7% and 3.7% in 2020 and 2021 respectively. With people returning to restaurants and fewer people working from home in 2022, processed food spending dropped 4% in 2022. Lockdown measures and consumer wariness to return to in-person dining caused spending on food service to contract 21% in 2020. Food service spending grew 23.5% in 2021 and another 9.8% in 2022, finishing the year 7.2% above 2019 prepandemic levels. The gains in folding carton demand reflected consumer spending trends. The restocking seen during lockdowns fueled a lot of the growth in shipments. While e-commerce supported some growth in folding carton demand, this will change in the medium term. Folding carton is best suited for shelves in brick-and-mortar stores. However, the shift to e-commerce for dry foods and non-food products could create a separate packaging and delivery channel, which could shift market share from recycled boxboard to corrugated packaging.

The COVID-19 pandemic and the associated recession saw spending shift from services to goods, which had a significant impact on folding carton shipments. While consumer spending in 2020 declined 3% and spending on services dropped 6.2%, nondurables spending increased 2.7%. In 2021, consumer spending rose 8.3%, with nondurables spending increasing 8.8%. Spending on services in 2021 saw a partial recovery, rising 6.3%. In 2022, spending grew 2.7% but began to shift toward services, which increased 4.5% for the year. While still elevated, non-durables good spending dipped 0.5% in 2022. Consumer spending on processed food witnessed strong growth of 5.7% and 3.7% in 2020 and 2021 respectively. With people returning to restaurants and fewer people working from home in 2022, processed food spending dropped 4% in 2022. Lockdown measures and consumer wariness to return to in-person dining caused spending on food service to contract 21% in 2020. Food service spending grew 23.5% in 2021 and another 9.8% in 2022, finishing the year 7.2% above 2019 prepandemic levels. The gains in folding carton demand reflected consumer spending trends. The restocking seen during lockdowns fueled a lot of the growth in shipments. While e-commerce supported some growth in folding carton demand, this will change in the medium term. Folding carton is best suited for shelves in brick-and-mortar stores. However, the shift to e-commerce for dry foods and non-food products could create a separate packaging and delivery channel, which could shift market share from recycled boxboard to corrugated packaging.

Additional headwinds include changing consumer behavior and the increasing demand for non-carton-intensive products, such as liquid soaps and detergents.

Economic uncertainty, lower levels of consumer spending on goods and an end to the inventory rebuilding cycle, which helped drive carton demand higher in 2021-22, will cause carton shipments to drop an estimated 3.8% in 2023. In the years that follow, however, macroeconomic indicators suggest that demand for folding cartons should continue its positive, albeit slow, growth. Over the forecast period of 2022-27, we estimate that folding carton demand growth will average 0.4% annually, reaching 5.4 million tons by 2027. We anticipate output growth in nondurables, which comprises many carton-packaged goods including processed foods, will expand 0.7% over the forecast. General economic fundamentals in the US economy, such as the unemployment rate, will remain strong. A potential recession is becoming more of a concern for the near future as inflation eats into consumer budgets, but growth will remain strong over the forecast, with consumer spending growing 1.7% in 2022-27. In addition to the overall economic performance, there are other factors that play an essential role in folding carton growth dynamics, such as shifting consumer spending habits, substitution away from plastic packaging and efforts to reduce packaging waste.

In 2020, Canadian folding carton shipments increased significantly by 3%, but decreased 0.3% in 2021 before jumping 3.7% in 2022. Tonnage volume reached 446,000 tons, translating to C$1.25 billion. The macroeconomic environment in Canada over the outlook will be supportive of carton shipment growth; however, the planned closure of a cartonboard mill in 2026 will reduce Canadian folding cartonboard capacity by nearly 30%.

In 2020, Canadian folding carton shipments increased significantly by 3%, but decreased 0.3% in 2021 before jumping 3.7% in 2022. Tonnage volume reached 446,000 tons, translating to C$1.25 billion. The macroeconomic environment in Canada over the outlook will be supportive of carton shipment growth; however, the planned closure of a cartonboard mill in 2026 will reduce Canadian folding cartonboard capacity by nearly 30%.

This will greatly reduce the amount of folding cartons that can be produced and shipped in Canada. As a result, folding carton shipments are expected to decline by 2.7% per year over the next five years and fall to 388,000 tons by 2027.

On prices, the situation is somewhat challenging, particularly for independent converters, mainly due to cartonboard prices consistently outpacing actual folding carton prices for several years. To provide some perspective, market prices for cartonboard grades increased at a 5.1% average annual rate from 2012-22; over that same 10-year span, folding carton average values per ton increased by an average of 2.3% annually. Coming out of the recession, average carton values were relatively stable in 2009 and 2010, but average boxboard prices in 2010 were 5.3% higher than in 2008. After boxboard costs increased another 7.4% in 2011, converters were forced to raise folding carton prices to prevent any further margin erosion but only gained 2.3% in average carton values. From 2012-17, the folding carton average value per ton fell at an average of 0.5% per year, losing ground on boxboard prices, which grew at a 1.5% rate. Around 2014-16, the flood of folding boxboard entering the global market provided some temporary leverage to independent converters in price negotiations with suppliers. However, mill closures reduced capacity, and with demand and producer costs rising, boxboard prices shot up significantly, swinging the market back in favor of integrated producers and sellers of boxboard to the open market. Over the past five years (2017-22), prices have become a more significant challenge for independent converters, as boxboard prices grew at an average rate of 8.9% per year, while the average value per ton for folding cartons rose just 5.2%.

The US folding carton end-use markets can be grouped into three broad categories: growth, mature and declining. Growth markets are classified by average annual growth of 1% or more. According to our analysis, four end-use markets are poised to grow by more than 1% per year. Nine end-use segments are classified as mature markets and are expected to maintain current levels of demand over the five-year forecast cycle. The remaining four market segments are classified as a declining market this year. The end-use markets analyzed in the full 2023-24 Trends Industry Outlook & Market Data Report are:

Food products

- Beverages

- Cereals /milled grains

- Confectionary

- Dairy

- Dry foods

- Frozen foods

- Meat

- Perishable baked goods

- Retail carry-out

Non-food products

- Cosmetics & toiletries

- Hardware & household supplies

- Converted paper products

- Pharmaceuticals

- Recreational & sporting

- Soap & detergent

- Tobacco

- Miscellaneous

The entire 2023-2024 Trends Industry Outlook & Market Data Report for the folding carton industry is available through the Paperboard Packaging Council (PPC). For over 90 years, PPC has been the North American association for converters of paperboard packaging and their suppliers. PPC works to grow, promote, and protect the paperboard packaging industry while providing its members with resources and tools to compete successfully in the marketplace. For more information, call 413.686.9191 or visit www.paperbox.org.