How the sense of touch creates physical and emotional experiences that engage customers, drive sales and build brand loyalty.

By Vicki Strull, design strategist, Vicki Strull Consulting

As designers, marketers, printers and converters, most of us can’t help but think about the power of touch when we think about the essence of print marketing and packaging. Over the past several years, the latest research attests to the relationship between touch and human emotional connection. The importance of special effects and embellishments for the entire print and packaging industry can be summed up quite simply: touch creates memorable customer experiences that build connection, sales and brand fans.

The Neuroscience of Touch

There are dozens of studies on the sensory connection of touch. Neuroscientists have discovered that more than half of our brain energy is devoted to processing sensory input. The part of the brain that receives input from our sensory receptors is called the somatosensory cortex, and a significant portion of that is devoted to our sense of touch.

Findings like these are revealed in “The Neuroscience of Touch,” an extensive piece on “neuroscience, communication, paper, persuasion and touch,” conducted by Sappi North America in conjunction with neuroscientist Dr. David Eagleman. ¹ For example, one of the questions explored in the research is whether or not we remember content differently when we read it digitally (such as online or on an iPad or Kindle) vs. when we read it on paper (such as a newspaper, catalog, magazine or book).

When we consume content online, we tend to read or scroll pretty quickly. But when we read something on paper, we engage in touchpoints, such as folding down a page or marking an item or highlighting a passage. Actions like these help us remember the content better, longer and more accurately. That’s the mental sensory mapping that occurs in our brain when touch is involved. The answer is yes, we do remember content we read on paper better than content we read online.

Following that study, researchers began to wonder if the medium of paper itself could explain the memory advantage of print vs. digital. Turns out, that is exactly what makes the difference. One theory is that the physicality – the realness of print and packaging – has a powerful effect on how we comprehend and retain messages, as compared to digital mediums. ² And, because more parts of our brain are activated when we are touching or holding a printed piece or packaging, we again are creating stronger memories and remembering the content better.

Touch, Texture and Trust

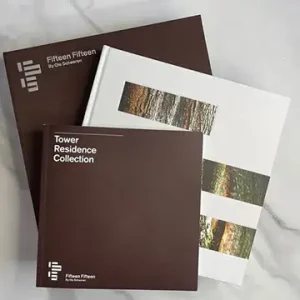

This tactile research also applies to substrates, special effects and embellishments. A texture on a package may encourage someone to take it off the shelf or hold it a little longer. That kickstarts a connection to the product or brand that is both physical and emotional. It affects our perception of the product’s quality and value, too. And since research shows that 95% of our purchasing decisions are subconscious and based on emotions ³, you can see how haptics drive sales. One more important finding is that because paper and paper-based packaging have a tangible quality – that realness mentioned above – humans also put greater trust in it. And trust is essential to building brand loyalty.

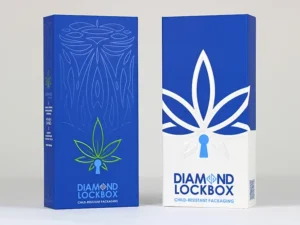

Recently, Sappi partnered with Clemson University to undertake a series of custom research studies to compare premium packaging and non-premium packaging to see which sold better. For the studies, premium packaging was defined as printed on Sappi’s Spectro®, a solid bleached sulfate (SBS) paperboard of the highest quality, and with at least one special effect or embellishment – namely metallic foil, spot gloss or embossing. Non-premium packaging was defined as printed on coated recycled board (CRB), typically used for household goods or nonfood-contact dry food packaging, such as cereal, crackers or processed foods.

To test the comparison, 60 participants shopped in a mock retail store. One data point became very clear: people overwhelmingly chose the premium packaging over the plain. They touched it, held it, turned it over in their hands. Specifically, 93% of people chose to purchase premium; they also chose the packaging with metallic foil 50% more often than any other packaging.

“The Packaging is the Product.”

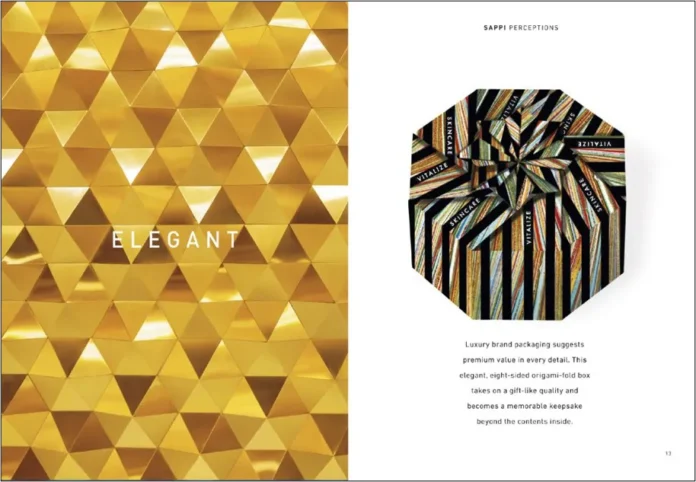

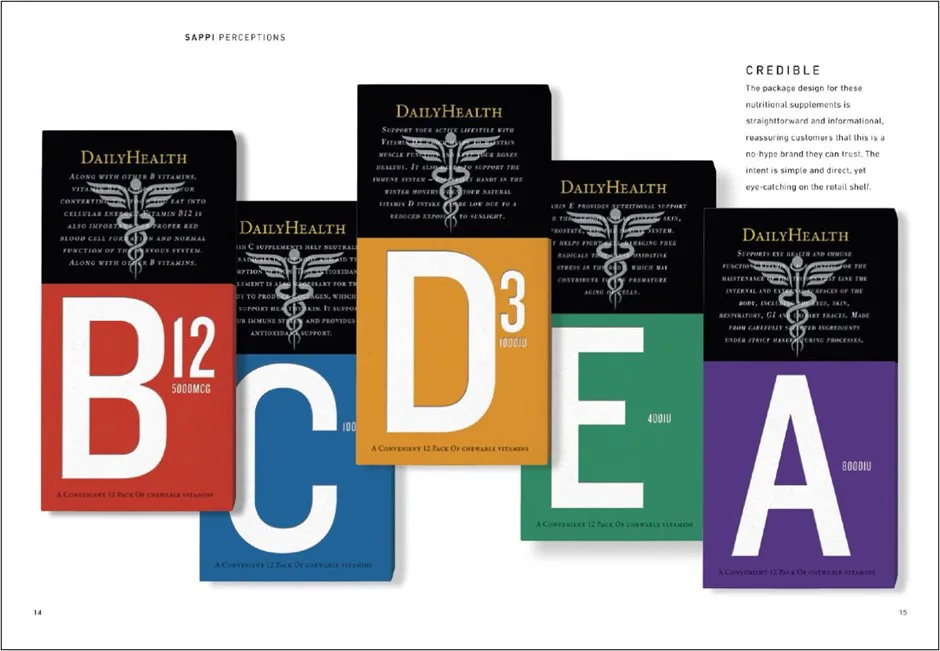

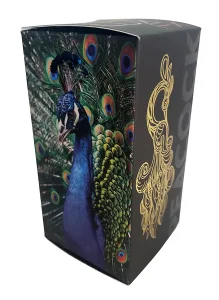

Twentieth-century graphic designer Saul Bass liked to say, “The packaging is the product.” For examples, see Sappi’s Standard 7, “A Guide to Designing for Print: Tips, Techniques and Methods for Achieving Optimum Printing Results.” On one page, a brand that uses a uniquely shaped box with subtle color and jewel-like metallic foil creates a sense of elegant luxury beyond the product itself. On another page, a package with bold typography, pearlized graphics and straight-forward information offers the credibility of a high-quality brand that reassures shoppers. In another instance, a package with muted gradations and a spot gloss wave pattern evokes serenity and tranquility. All of these examples show how packaging becomes the product, how it reflects the brand and how it creates a positive perception that gives the consumer confidence, builds trust and creates a memorable customer experience so people will choose that brand. Sensory embellishment can drive that.

Although multiple techniques are both inspiring and effective, the Sappi and Clemson study showed that even just one embellishment, just one special effect, can have a very big impact on consumer behavior and conversion.

Outside the Box: From Packaging to Other Touchpoints

The data regarding the power of touch and the influence of haptic techniques also are relevant to general commercial print, marketing materials, direct mail, catalogs, magazines, hang tags and book covers. Marketers and printers recognize that these various touchpoints are all critical for creating a comprehensive customer experience of a product or brand. Consistency of design, story, color, quality and imagery across the digital and print world is imperative. Everything needs to work together as an integrated, omnichannel marketing strategy, with a cohesive look and feel, while sensory print and packaging reinforce the entire branding ecosystem and enhance the human emotional connection.

With today’s competitive marketplace, brands continually are looking for new and more powerful ways to connect with their consumers and create memorable experiences. While digital may be an early impression consumers see via e-commerce or online ads, print marketing materials and packaging drive the connection, the engagement, the influence and the sale.

Vicki Strull has more than 25 years of experience in the marketing and design industry as a brand strategist, creative director and packaging designer. She has advised both emerging and top-tier brands, such as Sappi, HP, Bayer, Coppertone, Pizza Hut and Wildfare, on how to leverage the power of design and packaging to increase sales, create new revenue streams and build brand loyalty. In addition to writing articles in global trade publications, Strull is an international speaker and an adjunct professor at Tulane University. Join fellow trendsetters at vickistrull.com or follow her on LinkedIn @vickistrull.

Reprinted with permission from Sappi.

See and feel how Sappi makes packaging come alive through “The Standard” by ordering your own copy at https://go.sappi.com/l/405492/2023-10-23/gnkx9c.

References

- Dr. David Eagleman is a neuroscientist, author, and adjunct professor at Stanford University.

- “How the Medium Shapes the Message,” study referenced by Dr. David Eagleman; see more at www.SappiPops.com

- Harvard Business School Professor Gerald Zaltman, Working Knowledge, “The Subconscious Mind of the Consumer (And How To Reach It)”

Lesley: During the pandemic, people found new ways to spend their time and money, and people really got back into collecting. And, I predict the market will continue to increase and remain steady over the next 10 to 20 years for sure.

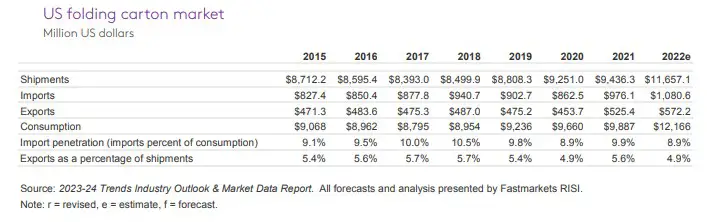

Lesley: During the pandemic, people found new ways to spend their time and money, and people really got back into collecting. And, I predict the market will continue to increase and remain steady over the next 10 to 20 years for sure. In 2022, as the world began to move past the COVID-19 pandemic, there were concerns about how markets would react as the economy moved toward a ‘new normal.’ Carton shipment growth had been in decline since the Great Recession. Prior to 2020, losses in shipments largely were the result of continued headwinds facing major processed food and consumer product companies. Processed food exports were challenged by the appreciation of the US dollar in 2015, which trickled down to recycled boxboard demand and folding carton shipments. Over the last decade (2010-19), folding carton shipments were under persistent downward pressure and declined at an average annual rate of 1.2%. Since the Great Recession, only four years have not experienced a decline in shipments: 2014, 2017, 2020 and 2021. When COVID-19 hit in 2020, industrial production dropped 7.2% and consumer spending fell 3%. Consumers, however, flush with stimulus money and stuck in lockdown, greatly increased their spending on goods, helping boost carton shipments to some of the strongest years in recent history. Carton shipments recorded extraordinary growth of 5.5% year on year in 2020. These gains were maintained in 2021 when shipments grew another 0.2%. With the remaining pandemic restrictions lifted in 2022, spending started to shift away from goods and back toward services, but strong inventory rebuilding throughout the supply chain helped push shipments up another 4.5%. While 2022 had the highest volume of carton shipments since 2010, it still was 8.7% below the pre-recession peak in 2007.

In 2022, as the world began to move past the COVID-19 pandemic, there were concerns about how markets would react as the economy moved toward a ‘new normal.’ Carton shipment growth had been in decline since the Great Recession. Prior to 2020, losses in shipments largely were the result of continued headwinds facing major processed food and consumer product companies. Processed food exports were challenged by the appreciation of the US dollar in 2015, which trickled down to recycled boxboard demand and folding carton shipments. Over the last decade (2010-19), folding carton shipments were under persistent downward pressure and declined at an average annual rate of 1.2%. Since the Great Recession, only four years have not experienced a decline in shipments: 2014, 2017, 2020 and 2021. When COVID-19 hit in 2020, industrial production dropped 7.2% and consumer spending fell 3%. Consumers, however, flush with stimulus money and stuck in lockdown, greatly increased their spending on goods, helping boost carton shipments to some of the strongest years in recent history. Carton shipments recorded extraordinary growth of 5.5% year on year in 2020. These gains were maintained in 2021 when shipments grew another 0.2%. With the remaining pandemic restrictions lifted in 2022, spending started to shift away from goods and back toward services, but strong inventory rebuilding throughout the supply chain helped push shipments up another 4.5%. While 2022 had the highest volume of carton shipments since 2010, it still was 8.7% below the pre-recession peak in 2007. The COVID-19 pandemic and the associated recession saw spending shift from services to goods, which had a significant impact on folding carton shipments. While consumer spending in 2020 declined 3% and spending on services dropped 6.2%, nondurables spending increased 2.7%. In 2021, consumer spending rose 8.3%, with nondurables spending increasing 8.8%. Spending on services in 2021 saw a partial recovery, rising 6.3%. In 2022, spending grew 2.7% but began to shift toward services, which increased 4.5% for the year. While still elevated, non-durables good spending dipped 0.5% in 2022. Consumer spending on processed food witnessed strong growth of 5.7% and 3.7% in 2020 and 2021 respectively. With people returning to restaurants and fewer people working from home in 2022, processed food spending dropped 4% in 2022. Lockdown measures and consumer wariness to return to in-person dining caused spending on food service to contract 21% in 2020. Food service spending grew 23.5% in 2021 and another 9.8% in 2022, finishing the year 7.2% above 2019 prepandemic levels. The gains in folding carton demand reflected consumer spending trends. The restocking seen during lockdowns fueled a lot of the growth in shipments. While e-commerce supported some growth in folding carton demand, this will change in the medium term. Folding carton is best suited for shelves in brick-and-mortar stores. However, the shift to e-commerce for dry foods and non-food products could create a separate packaging and delivery channel, which could shift market share from recycled boxboard to corrugated packaging.

The COVID-19 pandemic and the associated recession saw spending shift from services to goods, which had a significant impact on folding carton shipments. While consumer spending in 2020 declined 3% and spending on services dropped 6.2%, nondurables spending increased 2.7%. In 2021, consumer spending rose 8.3%, with nondurables spending increasing 8.8%. Spending on services in 2021 saw a partial recovery, rising 6.3%. In 2022, spending grew 2.7% but began to shift toward services, which increased 4.5% for the year. While still elevated, non-durables good spending dipped 0.5% in 2022. Consumer spending on processed food witnessed strong growth of 5.7% and 3.7% in 2020 and 2021 respectively. With people returning to restaurants and fewer people working from home in 2022, processed food spending dropped 4% in 2022. Lockdown measures and consumer wariness to return to in-person dining caused spending on food service to contract 21% in 2020. Food service spending grew 23.5% in 2021 and another 9.8% in 2022, finishing the year 7.2% above 2019 prepandemic levels. The gains in folding carton demand reflected consumer spending trends. The restocking seen during lockdowns fueled a lot of the growth in shipments. While e-commerce supported some growth in folding carton demand, this will change in the medium term. Folding carton is best suited for shelves in brick-and-mortar stores. However, the shift to e-commerce for dry foods and non-food products could create a separate packaging and delivery channel, which could shift market share from recycled boxboard to corrugated packaging. In 2020, Canadian folding carton shipments increased significantly by 3%, but decreased 0.3% in 2021 before jumping 3.7% in 2022. Tonnage volume reached 446,000 tons, translating to C$1.25 billion. The macroeconomic environment in Canada over the outlook will be supportive of carton shipment growth; however, the planned closure of a cartonboard mill in 2026 will reduce Canadian folding cartonboard capacity by nearly 30%.

In 2020, Canadian folding carton shipments increased significantly by 3%, but decreased 0.3% in 2021 before jumping 3.7% in 2022. Tonnage volume reached 446,000 tons, translating to C$1.25 billion. The macroeconomic environment in Canada over the outlook will be supportive of carton shipment growth; however, the planned closure of a cartonboard mill in 2026 will reduce Canadian folding cartonboard capacity by nearly 30%.

Prepared for PPC members by RISI, a provider of pulp and paper industry intelligence, the Trends Report describes how overall economic trends will affect the folding carton market in the near and far terms. The report states that general economic fundamentals in the US economy will remain strong throughout the coming years, for example, with consumer spending growing by 1.8% from 2021-26.

Prepared for PPC members by RISI, a provider of pulp and paper industry intelligence, the Trends Report describes how overall economic trends will affect the folding carton market in the near and far terms. The report states that general economic fundamentals in the US economy will remain strong throughout the coming years, for example, with consumer spending growing by 1.8% from 2021-26. We all like to feel we are part of a select few; that we have come across something rare and handcrafted – that we are one of the lucky ones to get our hands on it. While by no means purely handmade, Singer sewn and exposed Smyth binding convey this feeling to clients and consumers, and that’s what matters.

We all like to feel we are part of a select few; that we have come across something rare and handcrafted – that we are one of the lucky ones to get our hands on it. While by no means purely handmade, Singer sewn and exposed Smyth binding convey this feeling to clients and consumers, and that’s what matters. 2. High-end binding

2. High-end binding 3. Haptic

3. Haptic While scented inks have been around for a while, they now are– finally – trendy, from offering an intriguing aroma right out of the box to “scratch-and-sniff” or Rub’nSmell options. Depending on the effect desired, the scent can be added to the coating or varnish and thus applied inline with the print run.

While scented inks have been around for a while, they now are– finally – trendy, from offering an intriguing aroma right out of the box to “scratch-and-sniff” or Rub’nSmell options. Depending on the effect desired, the scent can be added to the coating or varnish and thus applied inline with the print run. A 2020 McKinsey study found that personalization will be the prime driver of marketing success within five years. Which means, we are just in time.

A 2020 McKinsey study found that personalization will be the prime driver of marketing success within five years. Which means, we are just in time. Sustainability is an overarching trend – one that goes beyond recycled paper but encompasses the whole printed piece. No, this trend does not sparkle or shimmer, but I encourage you to be aware of the sustainability, recyclability, etc. of the papers, printing and finishing techniques and embellishments you offer.

Sustainability is an overarching trend – one that goes beyond recycled paper but encompasses the whole printed piece. No, this trend does not sparkle or shimmer, but I encourage you to be aware of the sustainability, recyclability, etc. of the papers, printing and finishing techniques and embellishments you offer.