By Mark Porter, president, Dienamic Software

Costs are important to every business. Probably the most important equation in any business is:

Sales – Costs = Profits

Costs must be calculated to determine profits. Sure, at the end of the year, businesses can add up all of their bills and invoices to determine if they made a profit. But if there is detailed data of costs and production data, that information can be leveraged to make decisions on individual jobs, machines and people throughout the year that will maximize those profits.

Employee costs aren’t just direct wages; they get benefits and vacations. They aren’t always busy doing what they are paid to do. There are people who have to be paid to run the office. There are many costs that must be accounted for throughout the year.

Machines aren’t just the cost of the machine: There are financing charges; the machine takes up floor space and electricity; and they require certain materials that can’t be charged back to a specific job. It takes employees to run the machines, and the machines must absorb part of the rent, taxes, electricity, insurance, depreciation and so on. The machines must be assumed to work so many hours a week and; if things are slow, that can affect costs. Running one, two or three shifts can affect the cost of a piece of equipment.

The benefit of taking the time to calculate these costs and apply them to daily operations allows for making decisions daily to maximize profits – not just hoping and wishing for profits at the end of the year.

Estimating vs. selling: Not every job equals profit

Very few finishers or binders know what their machines actually cost per hour. In fact, the vast majority of businesses use selling rates per hour for their machines. They know they can get $100/hour for that machine or that they can get $45/m – again, a selling value. This puts them at a huge disadvantage. Imagine how much more profit they would make if they could determine their most profitable work – especially when they are busy. Sales efforts and machine usage should be directed to this type of work.

Businesses need to be aware of the concept that estimating and selling are two different functions. Most companies respond that the market dictates the price. This is absolutely true, but the market does not dictate costs to produce the job. It doesn’t stop companies from evaluating if this job, at the market price, covers their costs and provides the desired return (Table 1).

Costs are determined by production standards achieved in the plant. This data can be obtained through a variety of different methods that will be discussed shortly. The standards then can be multiplied by hourly cost rates that accurately reflect the cost of running the machines on an hourly basis. These rates are called budgeted hourly rates (BHR), and there are different ways to calculate them. They encompass all the costs listed previously – machine cost, labor, sq.ft. allocation of rent, utilities, insurance and much more.

When these hourly rates are applied to the production standards that have been determined, companies will have an accurate representation of how much the proposed job will cost to produce. They now can evaluate the risk, set the desired return and markup the quote to determine the selling price. If the market will not bear the desired price, companies now have all the data required to evaluate at what price they are unable or unwilling to bid on jobs. There may be times to bid on jobs below cost – but they will know they are below cost.

Once time standards are established, it is vital to constantly monitor production processes to ensure they are consistent with the standards used when estimating. For example, if estimating the speed of the press at 5,000/hr but actually only achieving 4,000/hr on the shop floor, companies are losing money on the job as soon as they win it. Conversely, if estimating at 4,000/hr and actually achieving 5,000/hr on the shop floor, it means losing jobs that could have been produced profitably. This monitoring can be done through software that measures productivity and compares estimated vs. actual values for every estimate.

Cost accounting and management information systems are vital to any job-oriented manufacturing business (such as finishers and binderies), no matter how big or small. The results will be more data, allowing companies to manage their businesses in a more profitable manner.

Budgeted hourly rates (BHRs)

BHRs are determined by simply identifying all of the costs for each cost center in the plant. The purpose is to recover all costs incurred in the production, sales and administration of products. Companies have to be careful not to include costs that are not part of a production process and, conversely, not miss costs associated with a production process. Either error will cause the hourly rate to adversely affect profitability.

The process of determining BHRs begins with identifying the processes performed in the plant. Then determine and collect the related data. Just because ABC Finisher and DEF Finisher have the same folder does not mean they will have the same hourly cost rate. ABC Finisher may have paid cash for its folder, its facilities rent may be less expensive, it works three shifts and it hires less-skilled employees. This will lead to a lower cost per hour for ABC Finisher.

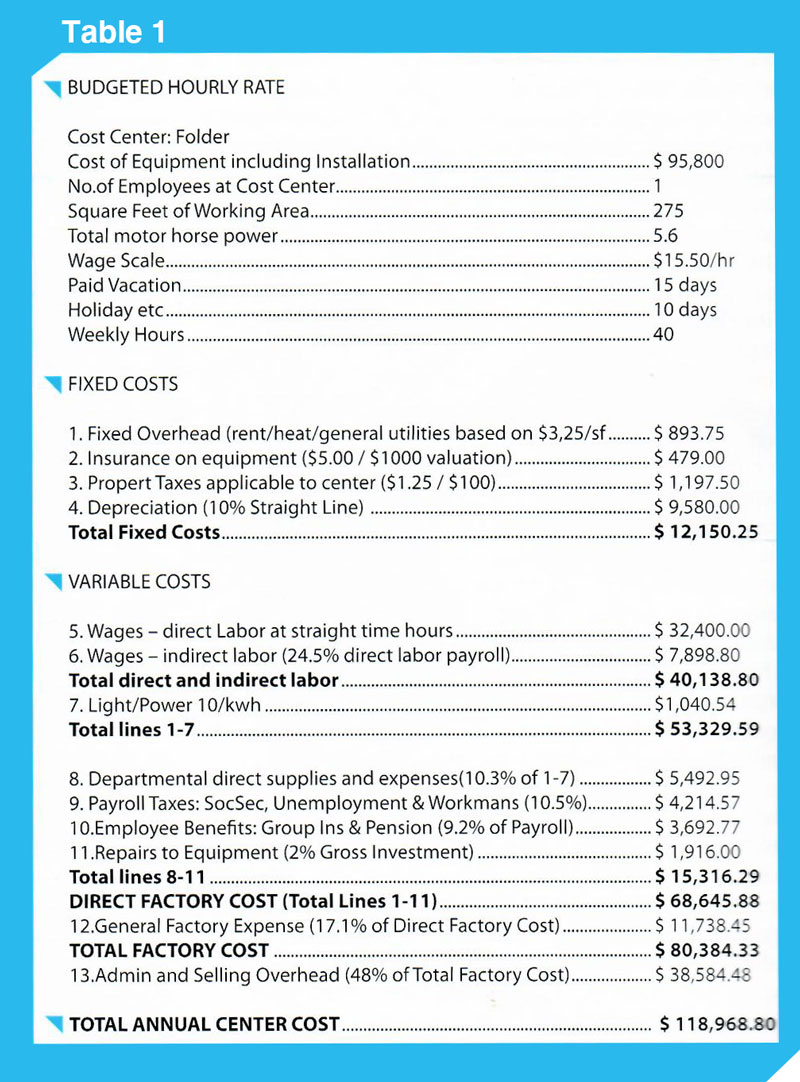

A sample BHR sheet for a folder is included to demonstrate the type of information that is required for the BHR calculation (See Table 1).

The Manufacturing Cost per Chargeable Hour is not the Budgeted Hourly Rate. It is useful if house errors must be charged back to the company (See Table 2).

The BHR reflects all costs incurred to produce the product, as well as the sales and administrative overhead. BHRs are not the prices. The calculation of the BHR multiplied by the time estimate should reflect the true cost to produce a product with no profit.

One note regarding overtime and multiple shifts: If a cost center is reaching 40% overtime, a second shift should be considered. The advantages of the second shift are the reduction of overtime and the ability to spread the fixed costs over a larger time block. This can result in substantial savings. Software is available to easily calculate BHRs based on industry-specific guidelines.

Production standards

The estimating system now has accurate hourly cost rates. The second piece of the puzzle is accurate production standards. Production standards are a measurement of output achieved on a certain machine by a certain employee under a certain set of circumstances.

A finishing or binding company can determine its production standards in six ways:

- Data Collection

- Intuition

- Published Results

- Competition

- Manufacturer

- Time and Motion Studies

Methods two through five use outside information that does not reflect actual conditions and, therefore, are of very little benefit. Method six is accurate but is very expensive and is not an ongoing process so not continually updated.

Method one represents the best method as it uses the company’s own data and is gathered in a continuous and real-time process that constantly reflects changes in output. Shop floor data collection devices are used to constantly send data to labor analysis and/or job costing software where the data can be sorted and analyzed by different jobs, machines and employees.

Production standards are used by the estimating system to provide the time element of the quote. Production standards constantly must be monitored to ensure the estimating department is using standards that accurately reflect the production capabilities on the shop floor.

Both components of the estimating system – BHRs and production standards – constantly can change. Equipment gets old, new employees with less or more skills start working and other factors change the production achieved. BHRs change with increases to rent or utilities, new equipment purchases and the addition of shifts.

A good system will allow for monitoring both components of the estimating system with an actual vs. estimate report for each job. This report will allow companies to see at a glance how they estimated the job compared to how it actually was produced. Any variations should be examined.

Weekly and monthly production analysis reports for both the processes and employees will allow companies to spot changes in production standards. This will ensure that the estimating system always is using the most accurate data and allow companies to obtain the type of work that can be produced with the most profit.

This is a good policy in good times and slow times. In good times, when there are never enough hours in the day, why work overtime to produce jobs that don’t provide a good return? In slow times, it is vital that the exact profit position be known when customers demand price cuts. Software is available to easily help perform all these functions, leaving more time to manage the business in a way that is well informed and profitable.

The biggest cost in any postpress company is labor. Automated labor management systems can track every second of every employee and every machine to know exactly what those people and machines are doing. This is valuable and dynamic information that can be used to make vital decisions.

A labor management system allows companies to track employees’ chargeable and nonchargeable time. If an employee has only 50% of his time that can be charged against jobs, then the role of that person should be questioned. Companies can see how employees rank in order of productivity. Machines can be monitored as to how much time is spent on makereadies, running, waiting, repairing and maintaining – and investment decisions can be made. When adding the BHRs to this time, there now is valuable costing information to maximize profits.

Mark Porter is the president of Dienamic Software. Dienamic offers a wide variety of software products and services designed specifically for trade binderies and print finishers. For more information, call 800.461.8114 or visit www.dienamicmis.com.