by Dr. Ronnie H. Davis, senior vice president and chief economist

Printing Industries of America

With 2018 rapidly coming to an end, printers and suppliers are turning their attention to 2019. The Printing Industries of America (PIA) provides its outlook for the 2019 economy and print markets with a focus on the following:

- An update on current macroeconomic conditions and outlook for next year

- Current print market conditions

- 2019 print markets

Current macroeconomic conditions

The American economy was operating in high gear as of the third quarter of 2018. Signs of strength abound:

- Second-quarter gross domestic product (GDP) increased at a very robust pace of 4.2% on an annual basis.

- Core inflation continues at a low rate, although it is heating up.

- Consumer and business confidence remain very strong.

- Business profits are high, driven by strong domestic and global sales, plus deregulation and lower corporate taxes.

- Employment is growing, and the unemployment rate is extremely low, pushing up wages.

- Stock prices and home prices are growing.

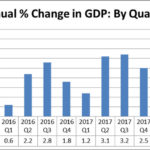

The 4.1% growth pace for the economy for the second quarter ranks as the highest mark out of the last 10 quarters going back to 2016. The current economic expansion started all the way back in June 2009, a phenomenal 112 months of sustained growth. This makes this expansion the second longest in 164 years of record keeping by the National Bureau of Economic Research, the official scorer of the economy. The only longer expansion was from 1991 to 2001, which commenced a discussion about the “new normal” and an end to the business cycle. Unfortunately, the Great Recession of 2007 to 2009 put an end to that belief.

PIA’s economic outlook for 2019

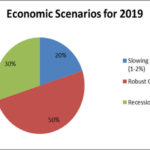

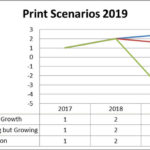

Will the strong economy continue into 2019? In our view, the economy will most likely continue on a pace of robust, above-trend growth of around 3% in 2019. However, as always, economic forecasting is fraught with uncertainty. As usual, we offer two other entirely possible 2019 economic scenarios:

- A “slowing but growing” trend line, with GDP retreating back to around 2% growth.

- A 2019 recession with total GDP down around 1.5%.

Other outcomes are possible, including higher growth or a more serious recession or any hybrid combination of the three scenarios. The likelihood of the three scenarios is a 50% chance for robust growth, 20% chance of slowing growth and 30% chance for a recession. Note, that we have increased the likelihood of recession from last year’s outlook from 25% to 30%. In our view, the likelihood will increase even more in 2020 if we get through 2019 without one.

Strong growth: This most likely scenario is a continuation of the recent uptick in economic growth. The two key drivers of this prospect are already in place – deregulation and the cut in corporate taxes. Both increase the competitiveness of the US economy and raise the equilibrium annual growth rate by around 0.5 to 1%. So far, the economy has been able to accelerate to this pace by an elastic response in labor force participation and a return to more “animal spirits” (instincts) in business investment.

Recession: Historically, most recessions are caused by two primary reasons – external shocks, such as oil shortages or a financial crisis, or excess exuberance leading to over-investment that finally results in cutbacks and downsizing. A variation of the second cause is simply the recovery dying of old age as new investment opportunities decline. A case can be made for either of these arising next year or in 2020.

At the present time the downside risks that could lead to a recession include:

- Trade restrictions or barriers that slow down the US/global economy.

- Labor shortages restrict growth, coupled with immigration restrictions (total number, quantity and quality, age). In the case of immigrants – will there be a substitute or complement to US labor supply?

- Bottlenecks – particularly in transportation.

- Costs and price pressures. Both are inherent in the growing economy and are also a result of possible missteps by the Federal Reserve as it unwinds the bond-buying push of the last few years.

- Interest rates ramp up from inflation, and increases in deficit crowd out private investment.

- Other wild card issues.

Slower growth: A slowing but growing economy would be a return to the economic trajectory of the past few years. The likely cause of this path is some combination of the six downside risks listed above. Just two or three of those in combination may not be enough to tip the economy into recession but certainly could shave a full point from the robust growth scenario and leave us with sluggish growth.

Current print markets

At the current time, print markets are robust, although, as always, they remain competitive. Generally, there are six key reasons why print and printers have largely been healthy over the last few years.

- Print has hit its sweet spot in the mature recovery phase of the economy.

- Most of the severe displacement of print by digital media is now behind us.

- Labels, wrappers and packaging print serve as an anchor on print sales, as it generally tracks very closely with the overall economy.

- Recently print marketing and promotion – particularly direct mail – has demonstrated its effectiveness as a premium marketing and promotional medium.

- Even the print sector most impacted by digital media – informational and editorial print (books, newspapers and magazines) – has been doing relatively well lately.

- Printers themselves have adjusted their business models to take account of new industry trends and realities.

On a nominal basis, print markets are growing around 1 to 2% at present. In total, the economic footprint for US print markets is very large:

- Approximately $170 billion in annual sales

- Over 800,000 employees

- Around 42,000 establishments

Printers’ profits are also generally healthy, based on historical trends. The most recent metric from PIA’s Ratios program shows profits as a percent of sales at 2.7%.

PIA’s print outlook for 2019

- So how will the three 2019 economic scenarios impact print?

- In the most likely robust-growth scenario (50% likelihood), overall print shipments increase by 2% or more next year. In terms of industry profitability, the average printer’s profit rate would likely increase by about 0.5% over trend to around 3.5% of sales.

- The recession scenario (up to 30% likelihood) would reduce total print and print-related shipments by around 2 to 4% next year. The typical printer’s profits would dip significantly into negative territory until the recovery is underway.

- The slowing-but-growing scenario (20% likelihood) would result in stable or slightly growing overall print sales in 2019. In this scenario, printers’ profits dip slightly to around 2.5% of sales.

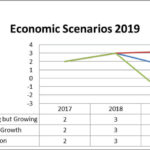

Printers’ profits: Printers’ profits will trend by significantly different paths, depending on the economic scenarios. In the robust-growth scenario, profits would jump significantly to historic highs of 3.4% of sales in 2018 and 3.5% of sales in 2019. If the economy falls into a recession, 2018 printers’ profits would be wiped out and turned into losses for both 2018 and 2019. In the trend scenario, profits would remain at 3% of sales for both 2018 and 2019.

Outlook by print processes: The current trends regarding print processes will continue in all three economic and print market scenarios. Three print processes that will grow relatively fastest over the next one to two years include: inkjet – both wide-format and production, wide-format – particularly digital and inkjet, and digital toner-based.

Outlook by print market segments: The current trends for specific print market segments also will likely carry over to next year in all three scenarios. Five specific print market segments will likely grow at a relatively higher rate than other sectors: packaging and specialty packaging, labels and wrappers, signage, direct mail and point-of-purchase.

In conclusion, most indicators point to a strong economy and healthy print markets next year. However, as always, printers and suppliers need to keep grounded and be ready to take advantage of the opportunities while at the same time looking out for the challenges.

Dr. Ronnie H. Davis is the Senior Vice President and Chief Economist of the Printing Industries of America. The PIA strives to enhance the growth, efficiency, and profitability of its members through advocacy, education, research, technical information and cost-saving resources. www.printing.org